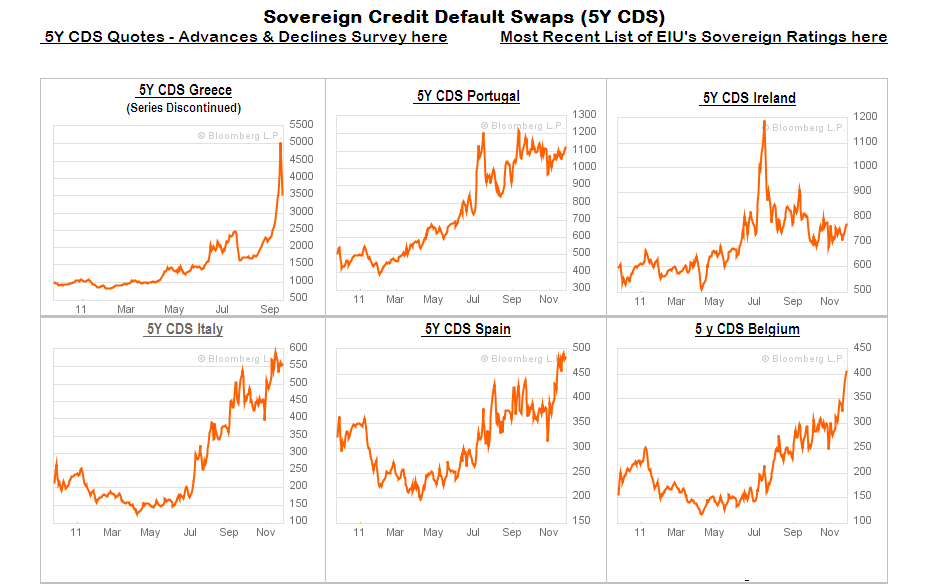

Recently there has been discussion about the fact that yields would have gone even higher had the ECB not been buying large quantities of Italian debt. This is something very disturbing because it tells just how much global investors have lost confidence in Italy's ability to serve its debt. All of a sudden people are percieving Italy as much riskier than they used to. So I asked myself: why is this happening? Why all of a sudden there is a lack of confidence in my countries' capability to remain solvent?

If we look at the Italian bond yield chart and we listen to what the news suggests (the English media in particular) we might come to the conclusion that this is the result of a sudden and unexpected problem. One might argue that bond yields surged this much because of uncertainty about the future of the Eurozone due to the bad financial situation that certain Eurozone sovereigns are facing. Although this factor was definitely one of the causes, I believe that it is not the only one. The problems are many and they are not only financial, but there are also political and social causes behind Italy's problems. Eventually all of this ended with Italy "losing its face" in the global environment because of media magnate Silvio Berlusconi's ackwardness and excessive italian-style humor that wasnt understood by the International press and political world, came at a wrong time and from the wrong person (you cant be a prime minister and a jester at the same time, even though it worked out to hook up the Italian voters) (Apparently). =P

Other causes that lead to he current situation are excessive legislative bureaucracy, which serves as an obstacle to the much needed FDI by slowing processes and "social division" between sustainers of Berlusconi and sustainers of the opposition, the socialist party, with the result of a country that isnt united, a problem for the country both at a national and international level. In the last elections Berlusconi won by a handful of votes. Almost half of the population wasnt happy with the previous ruling political party. This might be one of the causes of another major problem that Italy is facing, i.e. the loss in competitiveness of Italian firms in the global market. Eventually Berlusconi had to resign.

The new PM, Mario Monti, is the dean of Italy's most prominent economics university, an expert in economics and the financial markets.

I think that because the most important goal that Italy has to achieve right now is to lower its borrowing cost it is crucial that investors re-gain confidence in the Italian market and start re-buying Italian debt. The current yield level on 10yr bonds is unsustainable in the long term. Just think that an auction on November 29th commanded a 7.89% return on three-year bonds!

The appointment of a technocratic government was a first step towards the solution. Now it is up to Monti and his government to convince the markets further by imposing much needed austerity measures that will make him extremely unpopular in Italy but might be the only way to save Italy and Europe from the disaster that a breakout of the Eurozone would lead to in terms of GDP, real incomes, unemployment and inflation.

The new PM, Mario Monti, is the dean of Italy's most prominent economics university, an expert in economics and the financial markets.

I think that because the most important goal that Italy has to achieve right now is to lower its borrowing cost it is crucial that investors re-gain confidence in the Italian market and start re-buying Italian debt. The current yield level on 10yr bonds is unsustainable in the long term. Just think that an auction on November 29th commanded a 7.89% return on three-year bonds!

The appointment of a technocratic government was a first step towards the solution. Now it is up to Monti and his government to convince the markets further by imposing much needed austerity measures that will make him extremely unpopular in Italy but might be the only way to save Italy and Europe from the disaster that a breakout of the Eurozone would lead to in terms of GDP, real incomes, unemployment and inflation.